How Much Are Closing Costs In Ontario

Buying a home in Ontario is not just about paying the ticket price; there are several supplementary costs to consider, one significant one being closing costs. This often overlooked aspect of home buying can broaden your expenses and become a surprising addition to your budget. In this comprehensive guide, we will dive deep into the world of closing costs in the Ontario property market. Firstly, we will enrich your understanding of what constitutes Closing Costs in Ontario, thereby equipping you with the necessary knowledge. Secondly, we will delve into the various Factors that Influence Closing Costs in Ontario, providing key insights on how to anticipate these costs. Lastly, we will share valuable tips and strategies on effective Ways to Minimize Your Closing Costs in Ontario. As we lay the groundwork, let's first get our basics right by Understanding Closing Costs in Ontario.

Buying a home in Ontario is not just about paying the ticket price; there are several supplementary costs to consider, one significant one being closing costs. This often overlooked aspect of home buying can broaden your expenses and become a surprising addition to your budget. In this comprehensive guide, we will dive deep into the world of closing costs in the Ontario property market. Firstly, we will enrich your understanding of what constitutes Closing Costs in Ontario, thereby equipping you with the necessary knowledge. Secondly, we will delve into the various Factors that Influence Closing Costs in Ontario, providing key insights on how to anticipate these costs. Lastly, we will share valuable tips and strategies on effective Ways to Minimize Your Closing Costs in Ontario. As we lay the groundwork, let's first get our basics right by Understanding Closing Costs in Ontario.Understanding Closing Costs in Ontario

Understanding Closing Costs in Ontario is a crucial step in the home purchasing process. This essential process involves several key aspects, including The Basics of Closing Costs, Components of Closing Costs in Ontario, and The Importance of Estimating Closing Costs. Delving into the basics of closing costs, we unravel diverse elements associated with property transfer, including legal fees, land transfer taxes, and associated expenses specific to the Ontario real estate market. Next, understanding the various components that make up these closing costs in Ontario provides insight into how these fees can affect the overall purchase price of your investment. Lastly, recognizing the importance of estimating these costs accurately can prevent surprise expenses and offer a smoother transaction process. Armed with these crucial insights, Ontario homebuyers can better prepare and budget for their property purchase. Now, let's delve into our first topic: The Basics of Closing Costs. This section will lay the foundation for understanding the varied costs associated with closing a real estate deal, providing a broader picture of what to expect in the Ontario property market.

The Basics of Closing Costs

Understanding the basics of closing costs is a fundamental step in the home-buying process, especially in Ontario. Closing costs are the additional expenses you need to pay at the end of your real estate transaction. They can include items such as land transfer taxes, legal fees, home inspection charges, mortgage default insurance, if your down payment is less than 20%, and many more. The exact items and their costs may vary, which often makes it more complicated for homebuyers to understand. In Ontario, the average closing costs amount to between 1.5% to 4% of the purchase price of your home outside of your down payment. For instance, if your property costs $500,000, the estimated closing costs would be approximately $7,500 to $20,000, depending on several factors such as the amount of down payment, the tax in your municipality, the type of property and its location. It is crucial to account for these costs early in the process before making an offer on a property. The last thing you want to experience is an unpleasant financial surprise at the close of your home purchase. This process can be overwhelming, but the key lies in researching, budgeting, and asking your real estate agent or lawyer for a comprehensive list of what to expect. This way, you are well-prepared and can make informed decisions. Keep in mind, while these costs may seem daunting, they are a standard part of the home buying process. Your dream of owning a home in beautiful Ontario shouldn't be hampered by a lack of understanding of closing costs. With adequate knowledge, planning and, where necessary, negotiation, you can ensure that your closing journey is as smooth and straightforward as possible.

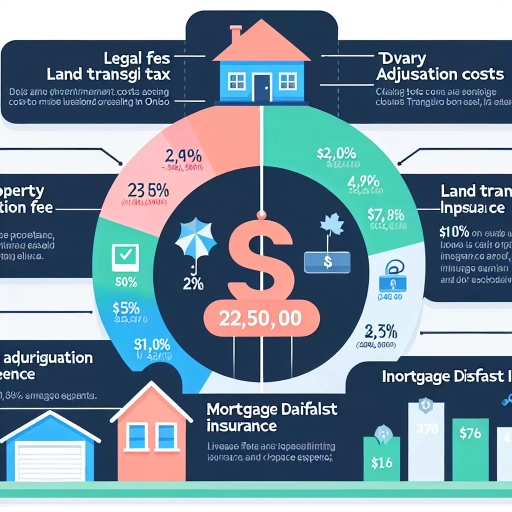

Components of Closing Costs in Ontario

Key components constitute Closing Costs in Ontario, which give a clearer picture of the overall expenditure involved for home buyers. Closing costs represent the array of fees that home buyers must pay at the end of a real estate transaction, and they become an unavoidable part of the property buying process. The average closing cost in Ontario ranges from 1.5% to 4% of the property's purchase value, with the final percentage depending on various circumstances such as the home location and the type of property purchased. The first component is Land Transfer Tax, a significant part of closing costs in Ontario. Ontario imposes this provincial tax on every property transaction, and Ontario's cities, like Toronto, impose an additional municipal tax. Calculating Land Transfer Tax involves a calculation-based tax rate applied on the property price. Next are Legal Fees and Disbursements, where you will need a lawyer to facilitate the transaction, performing tasks such as organizing important documents, conducting a title search, etc. Legal fees can vary widely depending on the complexity of the transaction and the lawyer's experience level. Other components include Title Insurance, vital to protect buyers from potential disputes. Home Inspection Fees, which varies according to the size, age, and type of property. Adjustments, which cover pre-paid costs by sellers such as property taxes and utilities. And Mortgage Insurance, mandatory when the down payment is less than 20% of the property's purchase price. Lastly, there might be other smaller factors such as moving costs, home insurance, and renovations among others. The above components can give you an insight into the extent of closing costs, but the exact breakdown can provide prospective buyers with a clear understanding of what lies ahead, enabling them to budget appropriately. Buying a home involves more than the listing price, and acknowledging these costs can prevent surprises down the line. Undoubtedly, experienced realtors and financial advisors can help navigate this terrain, making closing costs a manageable part of purchasing your dream home in Ontario.

The Importance of Estimating Closing Costs

The importance of estimating closing costs cannot be overstated when it comes to understanding closing costs in Ontario. These associated costs are a crucial determinant of your total expenditure while procuring a new property. By factoring these into the equation from the beginning, you ensure there are no unexpected surprises eating into your budget towards the end, thereby maintaining financial stability and preparedness. Closing costs comprise a diverse array of expenses, including but not limited to, Land Transfer Tax, title insurance, legal fees, and home inspection fees. Land Transfer Tax, in particular, is a significant consideration in Ontario due to its progressive structure. As the property's price increases, so does the tax rate, thereby making a detailed estimation of this cost vital for budgeting. Another aspect to consider is the legal fees that apply to title search, registration of the deed and mortgage, and the preparation of related documents. The cost varies according to the complexity of the deal, possibly running to thousands of dollars, underlining the need for estimation. Home inspection fees, though not legally mandatory, are highly recommended to discover potential issues with the property that might lead to costly repairs later. Moreover, with the increased cost of real estate in recent years in Ontario, high closing costs can further accentuate the financial burden on the buyer. Hence, an accurate estimation upfront assists in managing funds effectively and mitigating undue financial stress. Close monitoring and assessment of these costs can also serve as a valuable negotiation tool when finalizing the deal. In certain cases, the seller might agree to bear a part of these costs, adding another layer of advantage to precise estimation. In conclusion, the importance of estimating closing costs is manifold - it bolsters financial planning and preparation, facilitates smooth transactions, acts as a point of negotiation, and most importantly, it provides transparency in the intricate process of property acquisition. Understanding this piece of the puzzle is integral to comprehending the broader picture of closing costs in Ontario.

Factors Influencing Closing Costs in Ontario

In the intricate world of real estate transactions in Ontario, there are numerous factors contributing to the closing costs. The three main influencing elements being, the size and location of your property, lender's requirements, and significance of home inspections and appraisals in determining final costs. Firstly, it is without doubt that the size and geographical placement of your property draws a direct correlation to the closing costs - larger properties and those located in prime locations tend to carry higher costs due to increased value. The second factor to consider is the lender's requirements, which range from insurance to legal fees, and how these may influence the closing costs. Lastly, the essential roles of home inspections and appraisals cannot be undermined. These evaluations intended to assess the property's condition and value could significantly oscillate closing costs. As we delve into these aspects intimately, we must begin by understanding the relationship between the size of your property and its location, and how it ties into the closing costs scheme in Ontario's real estate market.

The Size of Your Property and Its Location

The size of your property and its location play a substantial role in influencing the closing costs in Ontario. Larger properties often have higher closing costs due to the increased complexities associated with transferring the property title and higher property taxes. For instance, when purchasing a larger property, there is typically more legal work involved, which can drive up lawyer fees. Larger properties also tend to need more profound inspections, which adds to the overall cost. For example, a property with multiple units, such as an apartment building or a commercial complex, would require a more extensive inspection than a single-family home, thus increasing the closing costs. In terms of location, properties in urban areas generally have higher closing costs than those in rural areas. One principal reason is the property taxes, often higher in urban districts due to higher property values and improved infrastructure. Additionally, city properties might encompass other costs like condominium fees if the property is a part of a shared building or gated community. These fees can significantly contribute to the overall closing costs being higher. Furthermore, the location of a property in relation to crucial facilities, such as schools, hospitals, and public transportation, can also influence its closing costs. Properties in prime locations often have higher property transfer taxes and levies than those in less-popular areas. If you are buying a property in such coveted locations, be prepared for higher closing costs due to these additional taxes. To sum up, while calculating closing costs in Ontario, it’s essential to factor in the size of the property and its location. These two factors significantly impact the overall closing expenses due to the additional legal work, property taxes, and other costs associated with the size and location of the property. Therefore, it's critical to evaluate and plan for these expenses when considering purchasing a new property.

The Lender's Requirements

Understanding the lenders' requirements is a critical aspect when considering the closing costs in Ontario. Lending institutions typically have set regulations that influence the final tally of these costs. Lenders effectively act as the gatekeepers to home purchases, making their demands integral in the transaction process. So, what exactly do these requirements entail, and how do they impact closing costs? First, lenders usually require a property appraisal. The appraisal, completed by a certified professional, estimates the value of the home to ensure that the lending amount matches the property's worth. This process is essential from the lending institution's viewpoint to mitigate financial risk. If for any reason the borrower defaults on their loan, the lender must be certain they can recover their losses through property sale. The cost of the appraisal, charged to the borrower, is a part of closing costs. Secondly, lenders often require title insurance to safeguard against title issues that might arise post-settlement. This coverage extends to problems like ownership disputes due to former liens or undisclosed heirs, thus offering protection to the lender's interests. The premium for this insurance is paid at closing and, thus, adds to the closing costs. The lender may also necessitate a property survey, especially in cases without a recent one. Such a survey defines property lines, easements, and land size to prevent any legal hassles about property limits in the future. But this too, while vital, adds to the closing costs. Lastly, some lenders have loan origination fees to cover administrative costs, such as processing, underwriting, and funding the loan. As with other requirements, this fee too becomes a part of the closing costs. All these lender requirements inevitably inflate the total closing costs, making it imperative for homebuyers in Ontario to factor them in. Understanding lender requirements hence becomes more than just a hurdle to loan approval - it's an integral element of discerning and budgeting for the final costs of home purchasing. To minimize surprises, potential homeowners should communicate with their prospective lenders, understand these specifications and account for them when estimating their overall closing costs.

The Role of Home Inspections and Appraisals

The role of home inspections and appraisals plays a significant part in the larger spectrum of factors that influence closing costs in Ontario. Home inspections are a critical phase in the home-buying journey that not only provides a detailed physical evaluation of your potential new property but also significantly impacts the negotiation process regarding the home's price. Typically, licensed professionals perform these inspections, evaluating the home's structure, systems, and overall condition, giving you a clearer understanding of your investment. Inspection costs can vary depending on the property's size and age, but buyers often consider it money well spent for the assurance it provides. On the other hand, an appraisal is a formal examination process done to assess a property's market value. Often required by mortgage lenders to ensure the cost of the house aligns with its real value, it influences the size of the mortgage loan you can be approved for. Appraisal fees are generally compensated to experienced appraisers who consider various elements, such as the home's features, location, and comparisons to recent property sales in the area, to generate an impartial market value. Both home inspections and appraisals are integral aspects of closing costs in Ontario. Understanding these processes better can aid potential homebuyers in estimating their closing expenses accurately, setting aside adequate funds, and ultimately making an informed decision. Given the dynamic real estate market in Ontario, being fully aware of these inherent costs can make a significant difference to one's financial planning and readiness.

Ways to Minimize Your Closing Costs in Ontario

Navigating the real estate market can be challenging, especially when facing the additional hurdle of substantial closing costs. This article aims to alleviate your worries by unraveling the complex facets of minimizing your closing costs in Ontario. We will first delve into the art of negotiation, where understanding and utilizing certain strategies can significantly lower your closing costs. Our journey will then take us through the maze of potential pitfalls that can unnervingly increase your closing costs, along with effective strategies you can implement to avoid these. Lastly, but equally as important, we will explore how you can benefit from Ontario's Home Buyer’s Plan and Land Transfer Tax Rebates. These financial incentives could be your life saver in expense-laden times. As you join us on this informative journey, we will equip you with essential knowledge, tips, and tools to navigate your closing costs with ease. Now, let's take the first step and dive into the world of successful negotiation, an invaluable tool in your quest to minimize your closing costs.

Tips for Negotiating Lower Closing Costs

When purchasing a property in Ontario, closing costs can ramp up rapidly and significantly impact your budget. However, there are negotiation tactics that can help in minimizing these costs. Firstly, it would be wise to compare and contrast different offers. Prioritize lenders who provide detailed loan estimates, ensuring transparency with the associated costs. A clear understanding of these costs can empower you to negotiate effectively. Secondly, scrutinize the 'junk fees.' These could include charges for administrative tasks such as processing, application, and courier, amongst others. Some such charges are unnecessary inflations and can be removed or reduced with successful negotiation. Request your lender to provide a breakdown of these fees and question the ones that seem illegitimate or excessively high. Thirdly, consider bundling the costs. A lender might be more open to lowering the costs if you agree to amalgamate certain aspects under one lump-sum fee. Be cautious, however, to ensure this doesn't disadvantage you in the long run. Seeking professional guidance can significantly boost your negotiation process. Real estate agents and attorneys have the necessary knowledge and experience to potentially negotiate better terms on your behalf. Lastly, it can be advantageous to negotiate your closing timeframe. A prompt closing can lessen your pre-paid daily insurance charges, thereby reducing your overall closing costs. By being proactive, conducting thorough research, and utilizing negotiation techniques, you can potentially lower your closing costs when buying a property in Ontario. Remember that expert advice and effective dialogue with your lender can result in substantial savings.

Avoiding Common Pitfalls That Increase Closing Costs

In your journey to home ownership in Ontario, it’s crucial to understand and circumvent the common pitfalls that often increase closing costs. Avoiding these traps doesn't just save you money but also economizes on time and reduces stress associated with the home buying process. The first common pitfall revolves around lack of proper legal support. Real estate transactions involve complex contracts and legal dealings. Many individuals underestimate the value that a knowledgeable real estate lawyer brings to the table. They can assist in detecting any hidden fees, potential legal issues in the contract, and also ensure a smooth transaction. Skimping on legal aid isn't advised as it might lead to higher costs should any legal problems arise. Secondly, failure to shop around for a mortgage is another pitfall. Given that the mortgage market is competitive, various lenders offer different interest rates and terms. Taking the first offer one receives might lead to higher long-term costs. It's always wise to take time, research, compare and negotiate to secure the most favourable mortgage terms. One more common mistake relates to skipping the home inspection. A comprehensive, professional inspection can spot potential issues with the property that might need costly repairs in the future. While it might seem like an additional upfront cost, it is a significant cost-saving measure in the long run. Lastly, not setting aside money for escrow fees can escalate closing costs. Many transactions involve escrow accounts, where the lender sets aside money for property taxes and insurance. Not having an escrow set aside might lead to penalties that can inflate the closing costs. In conclusion, understanding these common pitfalls is a proactive and strategic approach to minimize your closing costs in Ontario. Enlisting professional help, shopping for favourable mortgage terms, ensuring a thorough home inspection and setting aside money for escrow fees can significantly mitigate your expenses. This is an important part of the broader story about understanding and managing the closing costs in Ontario. By being informed and mindful of these factors, you can manoeuvre this process more cost-effectively, making your homeownership dream an affordable reality.

Benefiting from Home Buyer’s Plan and Land Transfer Tax Rebates

In your journey to minimize closing costs in Ontario, benefiting from the Home Buyer's Plan (HBP) and Land Transfer Tax rebates plays a crucial role. These cost-saving provisions have been put in place to support first-time home buyers, encouraging more individuals to invest in real estate and secure their future. The HBP is an initiative by the federal government that allows first-time homebuyers to withdraw up to $35,000 per person from their registered retirement savings plans (RRSPs) tax-free, to put towards buying or building a qualifying home. In essence, you're borrowing from your future self to finance your dream of owning a home today. The funds must be repaid within 15 years, but this still gives you a substantial cushion during the home-buying process, significantly reducing your immediate financial burden. On the other hand, the Land Transfer Tax can be a considerable part of your closing costs. The Ontario government recognizes this and offers rebates for first-time buyers. The Land Transfer Tax rebate can refund up to $4,000 of the tax paid by first-time homebuyers, effectively reducing closing costs, and in some instances even eliminating them entirely. For instance, if you buy a home for $368,000 or less, you won't have to pay the Ontario Land Transfer Tax. It's important to understand that the process of applying for the Home Buyer’s Plan and the Land Transfer rebate is filled with intricacies and technicalities. To fully benefit from these provisions, careful attention to details such as eligibility requirements and deadlines is necessary. Working with a knowledgeable real estate agent or lawyer can ease the process, ensuring you take full advantage of the potential savings these plans offer. Ultimately, these cost-saving strategies can make homeownership more affordable in Ontario, ensuring that purchasing your dream home doesn't lead to a financial nightmare. Easing the burden of the often-overlooked closing costs can help you manage your finances better, offering a smoother transition into your new home while laying the foundations for a secure financial future. Therefore, leveraging opportunities like the HBP and Land Transfer Tax rebates should not be overlooked in your strategy to minimize closing costs in Ontario.