Navigating the Loonie: Canada's 2026 Economic Outlook and Currency Forecast

By Aaron C. Zhang, Senior Forex Market Analyst

Resilience in a Fragmented World

The global macro environment is currently defined by a "profound rupture." Geopolitical competition, shifting industrial policies, and persistent conflict in the Middle East have fractured traditional trade routes and injected extreme volatility into energy infrastructure. Yet, as we navigate 2026, the Canadian economy is demonstrating an unexpected and sophisticated resilience.

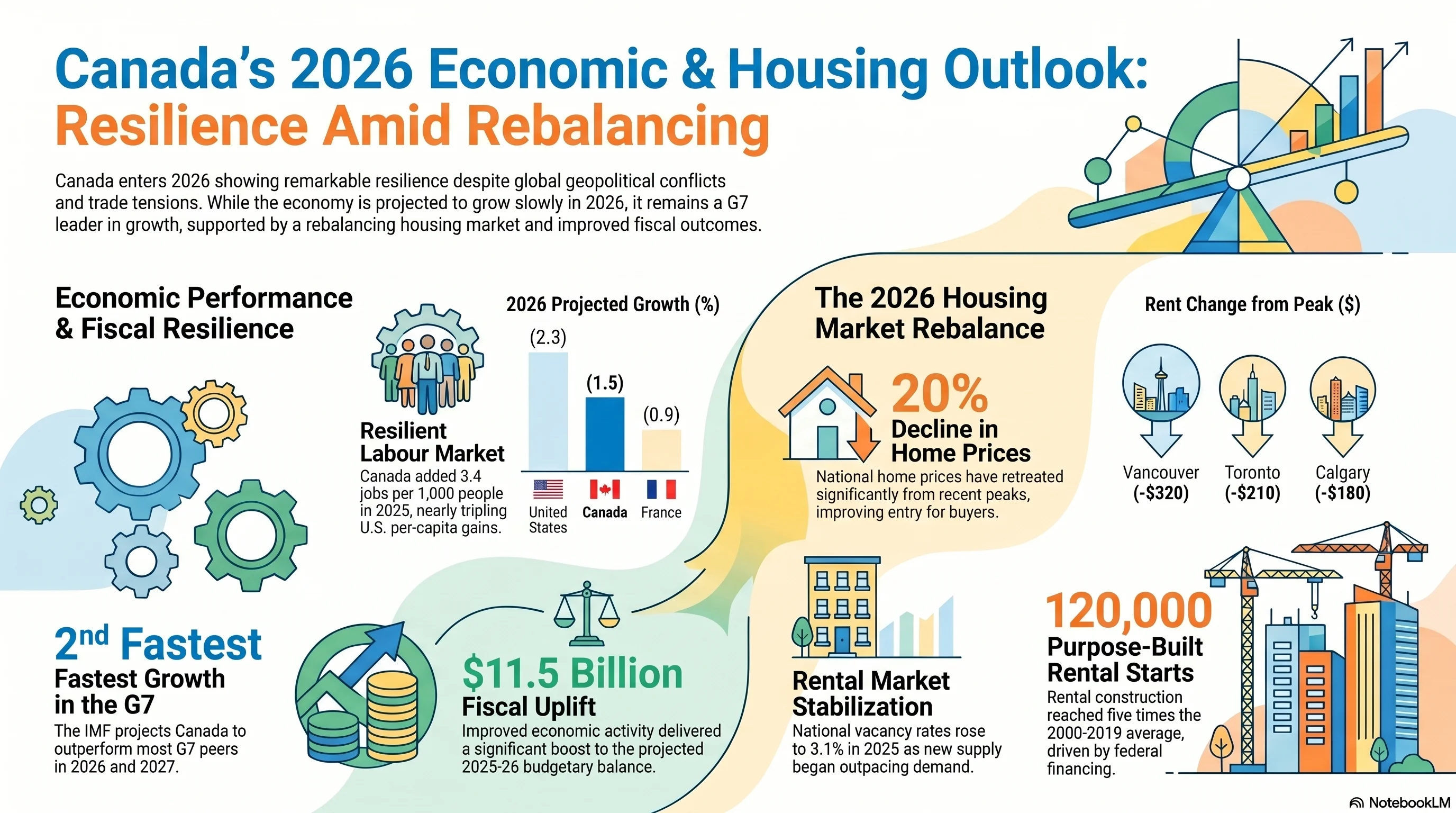

While global headwinds remain stiff, the core thesis for the Canadian "soft landing" remains intact. Following a robust 1.7% growth in 2025 that defied recessionary predictions, the Canadian economy is projected to stabilize further in 2026. This outlook is anchored by a rare AAA fiscal standing and a strategic pivot in population policy. For investors and currency observers, understanding the CAD's trajectory requires a deep dive into the divergence between Canadian and U.S. monetary policy, the structural rebalancing of the housing market, and the nation's burgeoning role as a stable energy provider in a risk-off world.

Watch: The Macroeconomic Stress Test — Canada's 2026 Economic Outlook

The Global Shock: Oil Volatility and CAD Implications

As a premier "petro-currency," the Canadian Dollar (CAD) remains tethered to the fortunes of the energy sector. The Middle East conflict has triggered a significant geopolitical risk premium, pushing oil prices into a range that bolsters Canada's terms of trade.

2026 WTI Crude Oil Price Trajectory

- Annual Average: Projected at US$80 per barrel (a US$15 premium over previous Budget 2025 estimates).

- Intraday Volatility: Market repricing has driven tactical peaks near US$120.

- Year-End Target: Futures curves suggest an easing to US$75 as shipping flows through the Strait of Hormuz normalize.

From a currency strategy perspective, the CAD is currently acting as a "geopolitical hedge." While the Greenback (USD) initially surged on safe-haven flows during the peak of the conflict, the CAD has consistently appreciated against non-USD peers. Higher energy revenues have provided a significant tailwind for government receipts and energy-sector profitability, helping to insulate the domestic economy from the broader global supply shock.

Growth and Inflation: The Path to Stability

According to the International Monetary Fund (IMF), Canada is set to retain its position as a growth leader within the G7. Crucially, the 2027 forecast confirms that Canada is not just experiencing a temporary bounce, but a sustained recovery.

| Nation | 2026 Real GDP Growth | 2027 Real GDP Growth |

|---|---|---|

| United States | 2.3% | 2.1% |

| Canada | 1.5% | 1.9% |

| Germany | 0.8% | 1.2% |

| France | 0.9% | 0.9% |

| United Kingdom | 0.8% | 1.3% |

| Japan | 0.7% | 0.6% |

| Italy | 0.5% | 0.5% |

Inflationary pressures remain a key focus for the Bank of Canada. A localized spike to 2.4% in March 2026 was largely "headline" noise, driven by a 30% surge in retail gasoline. However, core inflation—the Bank's preferred metric for underlying price stability—sat comfortably at 2.3% in the same period. This stability was aided by the federal government's temporary suspension of the fuel excise tax, which provided immediate CPI relief. Analysts expect headline inflation to revert to the 2.0% target by year-end as energy supply chains normalize.

Monetary Policy and Mortgage Rates: Managing the Yield Differential

The Bank of Canada (BoC) has successfully navigated a policy divergence from the U.S. Federal Reserve. By early 2026, the BoC had executed a cumulative 275-basis-point cut advantage over the Fed. This aggressive front-loading of cuts was designed to support the domestic "soft landing" by narrowing the yield differential and supporting credit markets.

The BoC is expected to hold its policy rate steady at 2.25% throughout 2026, though currency strategists are watching for a potential return of "carry trade" interest as the Canadian economy outpaces its European and Japanese peers.

Mortgage Watch

- Variable Rates: Expected to remain stable through early 2026 before rising mid-year as the BoC eventually normalizes the policy rate in line with strengthening domestic demand.

- Fixed Rates: Downward pressure is limited. Fixed rates are trending higher as 10-year bond yields average 3.4%. This is driven by term premiums returning to historical levels and increased government bond issuance to fund capital projects.

Big Six Banks: Interest Rate and Housing Forecasts

Canada's Big Six banks are divided on the 2026 rate path. Here is a summary of their key forecasts and rationales:

| Institution | Rate Forecast | GDP Growth | Inflation Outlook | Housing Predictions |

|---|---|---|---|---|

| BMO | Cut to 1.75–2.0% | 1.0%+ | Close to 2.0% with slight upward bias | Correction in ON & B.C.; Montreal & Quebec City strongest; Prairies stable |

| RBC | Hold at 2.25% | 1.3% | Around 2.0% target; core above 2.0% | — |

| CMHC | Hold / Normalize | 0.7% | — | Starts decline to 247K; sales at 489K; resale prices ~$698K avg. |

| CIBC | Hold at 2.25% | — | Downward pressure from soft economy | — |

| TD Bank | Hold at 2.25% | — | Close to 2.0%; slow growth balances costs | — |

| Scotiabank | Hike by 50 bps (to 2.75–3.0%) | — | Inflationary pressure from wages & weak productivity | Car & housing markets expected to pick up |

| National Bank | Hike by 50 bps (to 2.75%) | — | — | — |

The Great Housing Rebalancing: Regional Realities

Canada's housing sector is undergoing a profound structural adjustment. National home prices are down 20% from their post-pandemic peaks, while national rents have retreated 9% from their 2024 highs. The rental vacancy rate has expanded to a more functional 3.1%.

CMHC Regional Variance and Strategic Insights

- Ontario & British Columbia: These markets face the steepest headwinds. In Toronto, condo pre-construction sales hit multi-decade lows in 2025, leading to significant project delays. Conversely, Vancouver's rental vacancy rate has reached its highest level in over 30 years, signaling a shift toward a renter's market. Ontario remains the only province where price declines are expected to persist through 2026.

- Prairies & Quebec: These regions remain outliers of strength, with construction and sales activity holding well above historical averages due to superior affordability.

On the supply side, a gap remains. Housing starts are projected to decline to 247,000 units in 2026. While this is a drop from recent highs, it remains "historically elevated" compared to the 2000–2019 average of 200,000 units. However, this level is still insufficient to fully meet the demographic demand accumulated over the last decade.

The Demographic Shift: Moving Toward Sustainability

A critical component of Canada's 2026 stability is the pivot in population growth. Under the 2026–2028 Immigration Levels Plan, the federal government has moved toward a "sustainability" model.

Population growth, which peaked at a staggering 3.2% in 2024, plummeted to -0.2% by late 2025. This cooling of demographic pressure has allowed the labor market to find a new equilibrium and reduced the "housing supply gap" that plagued the economy in previous years. This easing of the "demand shock" is a primary reason why core inflation has remained anchored despite global energy volatility.

Fiscal Health: Canada's Sovereign Advantage

Canada's balance sheet remains the envy of the G7. This "Fiscal Advantage" allows the federal government to deploy temporary supports—like the fuel tax suspension—without threatening sovereign credit stability.

| Fiscal Metric | Canada | G7 Average (Excl. Canada) |

|---|---|---|

| Net Debt-to-GDP Ratio | 10.2% | 101.8% |

| Sovereign Credit Rating | AAA | Varies (Only DE holds AAA) |

The 2025–26 deficit is projected at $66.9 billion, a marked $11.5 billion improvement over previous forecasts, representing just 2.1% of GDP. This fiscal discipline is driven by a "Spending Less to Invest More" strategy, which includes $60 billion in savings from the Comprehensive Expenditure Review. Notably, the government is reining in external management and consulting services to find $900 million in annual savings, with the goal of having 100% of the deficit account for capital investments by 2028–29.

Key Takeaways for 2026

Canada enters 2026 as a bastion of relative stability. While the Middle East conflict and U.S. trade tensions present ongoing risks, the domestic economy has the fiscal and monetary tools to navigate the "profound rupture" of the global order.

Investor Takeaways

- Sustained Growth: Canada is projected to deliver the second-fastest growth in the G7 through 2027, driven by business adaptation and infrastructure investment.

- Currency Stability: A predictable 2.25% policy rate and the CAD's status as a geopolitical hedge make it an attractive "risk-off" commodity play.

- Market Rebalancing: The housing and labor markets are undergoing a necessary, healthy adjustment. Higher vacancy rates in Vancouver and lower price entry points in Ontario favor long-term economic sustainability.

Backed by its rare AAA credit rating and increasing energy export capacity via the Trans Mountain Expansion and new LNG projects, Canada remains a secure and reliable destination for global capital in an uncertain world.

Sources & References

- Big Six banks split on 2026 rate path. Here's what they think — BNN Bloomberg

- Canada's Growth Outlook Is Resetting – Policy Expectations Should Too — C.D. Howe Institute

- Canada's Population Estimates (2026Q1) — Shrink Nation — BMO Economics

- Economic Outlook: Insights Into 2026 — BMO Capital Markets

- Economic and fiscal overview | Spring Economic Update 2026 — Government of Canada

- Housing Market Outlook 2026 — CMHC

- Mortgage Rates Forecast Canada 2026–2030 — nesto.ca

- Steady as she goes – central banks hold the line in 2026 — RBC Economics

- The Impact of Mortgage Interest Costs on Rental Inflation Amid Population Growth — Bank of Canada / Publications Canada

- USD/CAD forecast 2026: Loonie recovery driven by rate differentials — FXStreet