Executive Summary

If you had told currency traders at the start of 2026 that the global economy was about to experience an unprecedented supply-side shock, most would have bet against the Canadian dollar. Yet, as the global financial landscape confronts a severe stagflationary impulse driven by an explosive Middle Eastern conflict, the Canadian dollar has shown remarkable resilience.[1,2] At the heart of this anomaly is the sheer psychological and technical gravity of West Texas Intermediate (WTI) crude surging past US$100 per barrel—a staggering threshold that translates to roughly C$140 per barrel.[3]

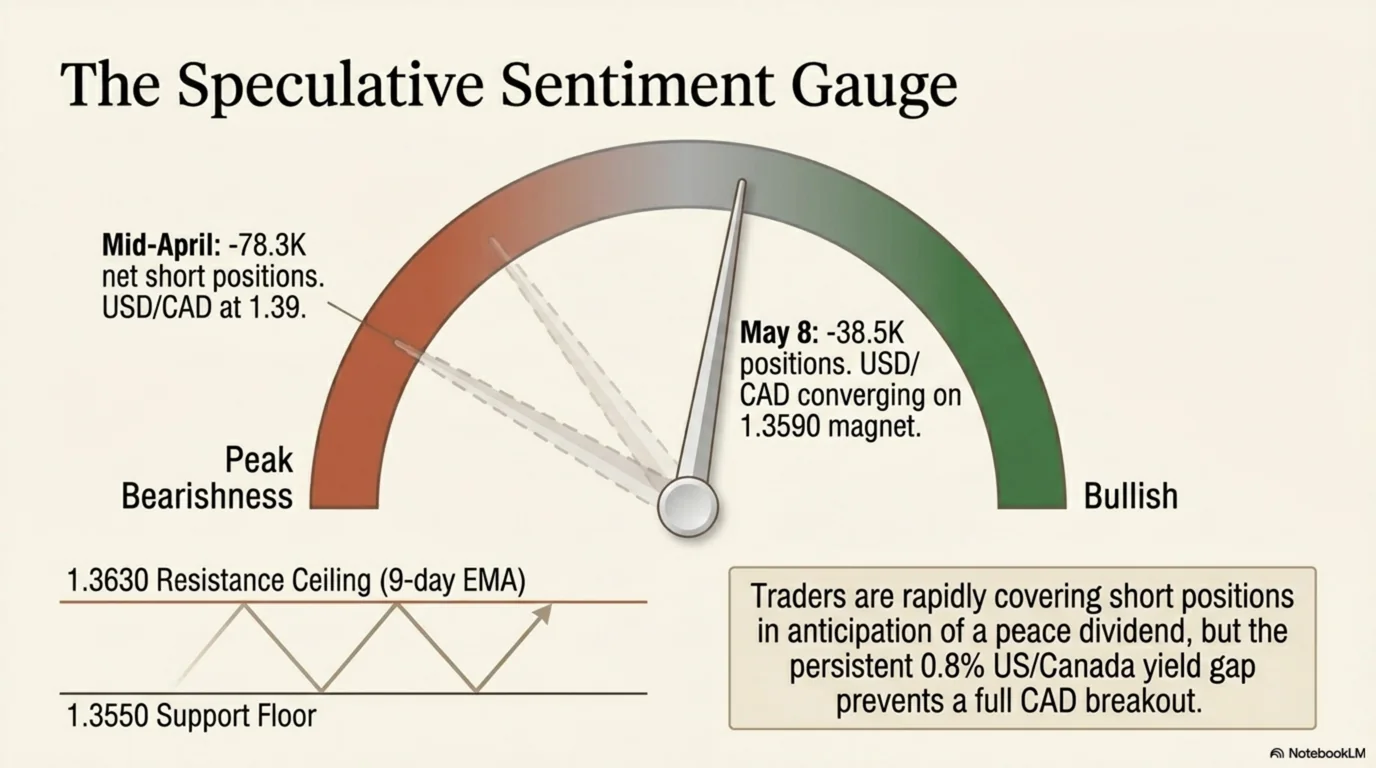

For currency markets, this threshold acts as a massive technical trigger. The USD/CAD exchange rate has drifted lower, marching steadily toward the critical 1.3500 convergence zone as the Loonie defies gravity.[4,5] As panic gripped global equities in March and April, the Canadian currency dug in its heels, supported by a rapid unwinding of bearish speculative bets.[6] Data from the Commodity Futures Trading Commission (CFTC) reveals that speculative net short positions on the CAD collapsed from a heavily crowded -78.3K in mid-April to just -38.5K by early May.[6–8] This sudden short-covering rally, combined with Canada navigating a tightrope between domestic economic burdens and massive fiscal tailwinds from a historic petro-windfall, explains the currency's strength.[1,6]

The Geopolitical Catalyst

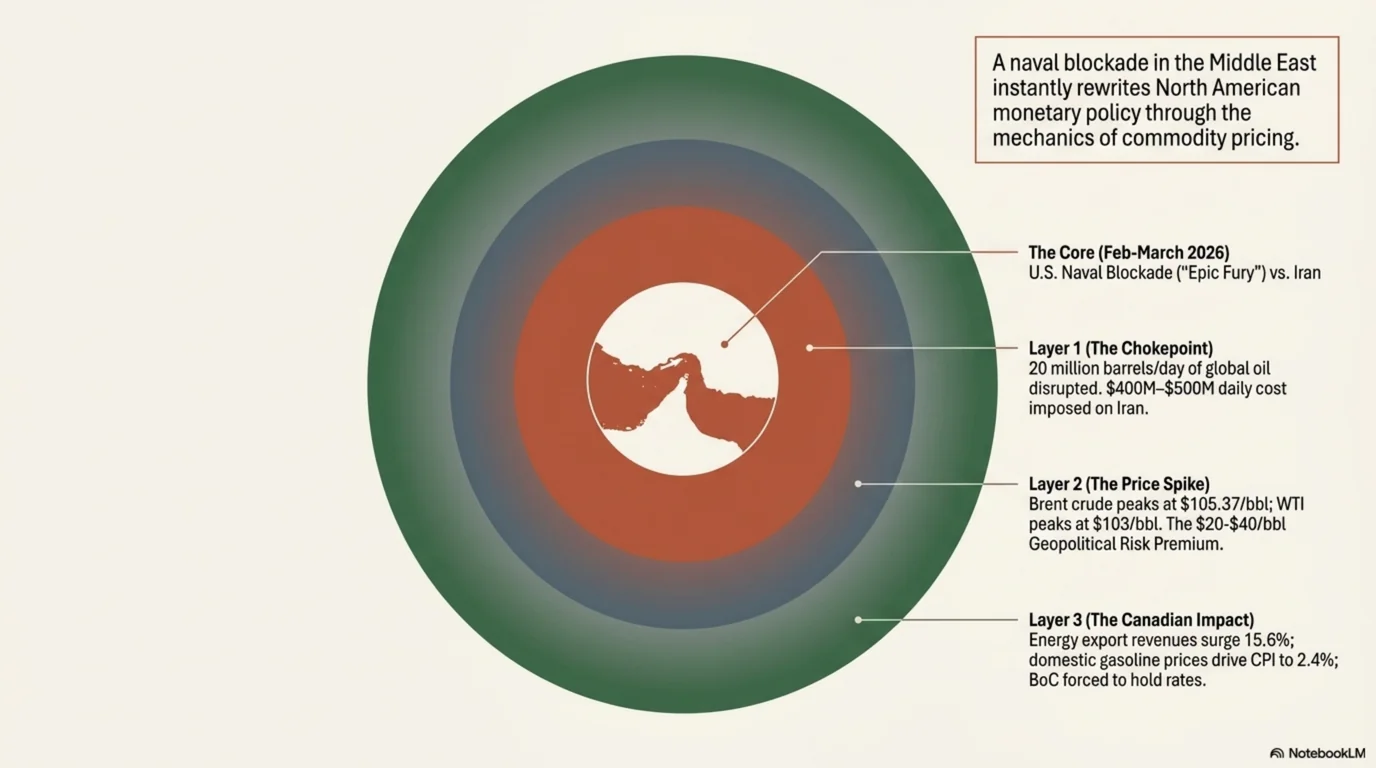

The genesis of the 2026 energy crisis began in late February with the rapid escalation of kinetic military actions involving the United States, Israel, and Iran.[1,9] When the Islamic Revolutionary Guard Corps (IRGC) retaliated by effectively closing the Strait of Hormuz, they blockaded a maritime chokepoint responsible for approximately 20% of the world's seaborne oil trade, paralyzing nearly 20 million barrels per day (mb/d) of crude and liquefied natural gas.[1,9,10] The United States countered with its own highly sophisticated naval blockade of Iranian ports, a maneuver branded by President Trump as "Epic Fury".[9,11]

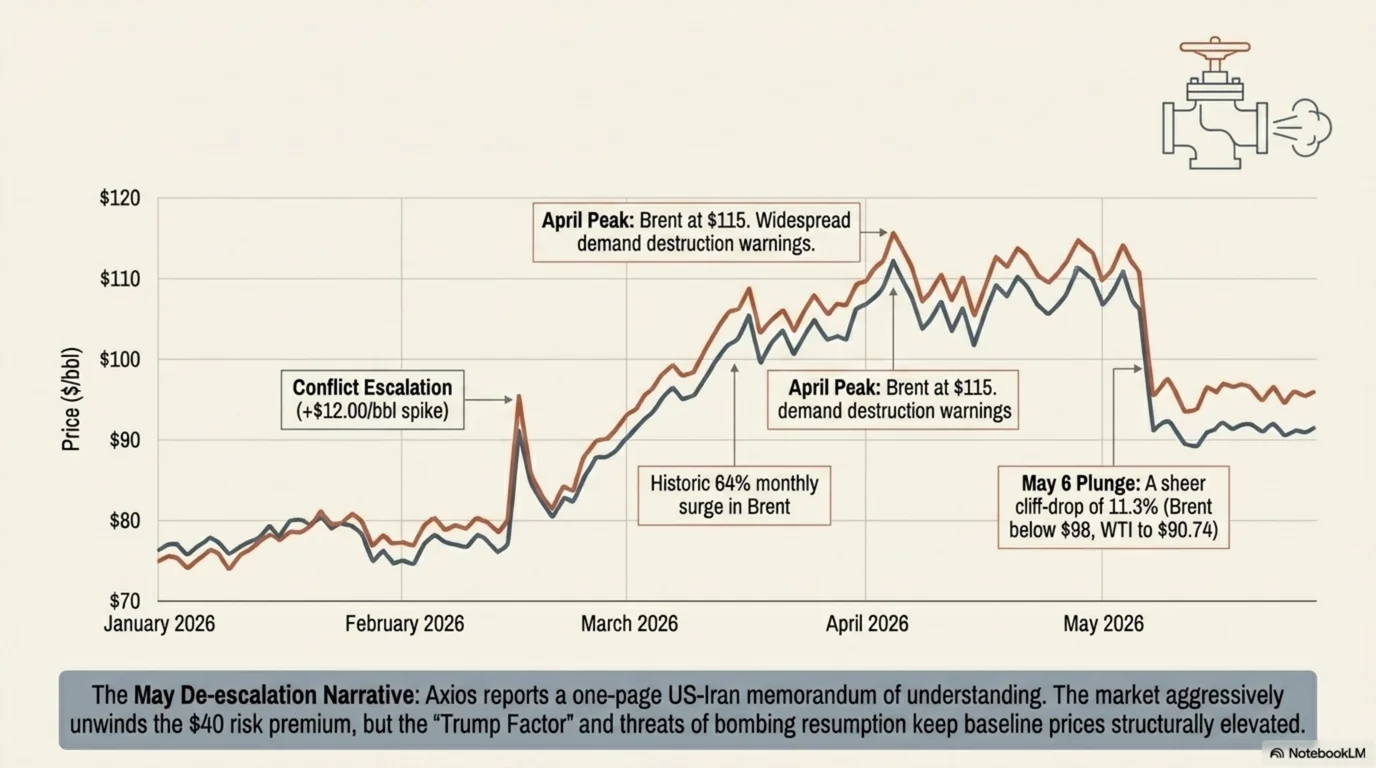

The reaction in the commodity futures markets was historic, with Brent crude experiencing a 64% monthly price surge in March.[3] At the peak of the panic in April, Brent futures topped $115 per barrel, while WTI spiked to $106.[2,3] Analysts quickly recognized that these inflated benchmarks contained a massive geopolitically-driven risk premium of $20 to $40 per barrel, reflecting skyrocketing shipping insurance costs, rerouting expenses, and physical scarcity.[3]

Why is this risk premium hitting the Canadian dollar differently in 2026?

- Safe-Haven U.S. Dollar Dominance: In a purely risk-driven shock, global capital floods into U.S. Treasuries, drastically strengthening the U.S. dollar against almost everything.[8] The overwhelming safe-haven appeal of the greenback has acted as a powerful counterweight, suppressing the Canadian dollar's natural upward momentum from oil.[8]

- The Brent-WTI Spread Advantage: Because the crisis is concentrated in the Persian Gulf, European and Asian markets bear the brunt of the physical scarcity, pushing the Brent-WTI price spread to a massive $15 per barrel in April.[12,13] While global markets starved, North American refiners remained relatively insulated, accessing cheaper domestic WTI crude while selling refined petroleum products at globally inflated prices.[14]

- Muted Domestic Capital Expenditure: Historically, a $100+ oil environment would trigger massive capital expenditure in the energy sector, but because the current price surge is viewed as a fragile geopolitical anomaly, investment in the Canadian oil and gas sector has remained surprisingly modest.[15,16]

The Trade Balance Shield

To truly grasp how the Loonie is defying gravity, you have to look at the Canadian merchandise trade ledger for March 2026, which is a masterclass in the mechanics of a "Petro-currency." Before the spring, the Canadian economy was flashing warning signs: the fourth quarter of 2025 saw a contraction in real GDP, housing activity declined, and the labour market exhibited softness with the unemployment rate stuck in the 6.5% to 7.0% range.[17,18]

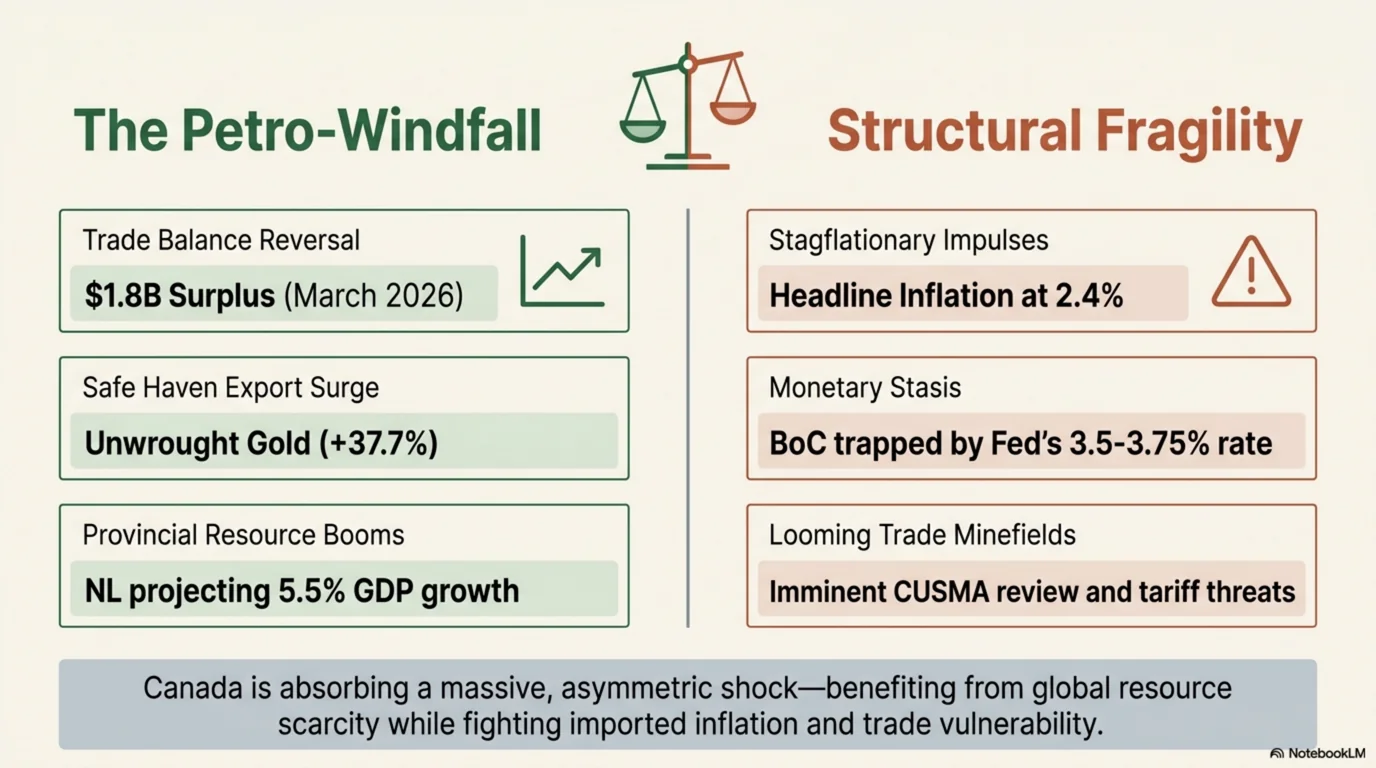

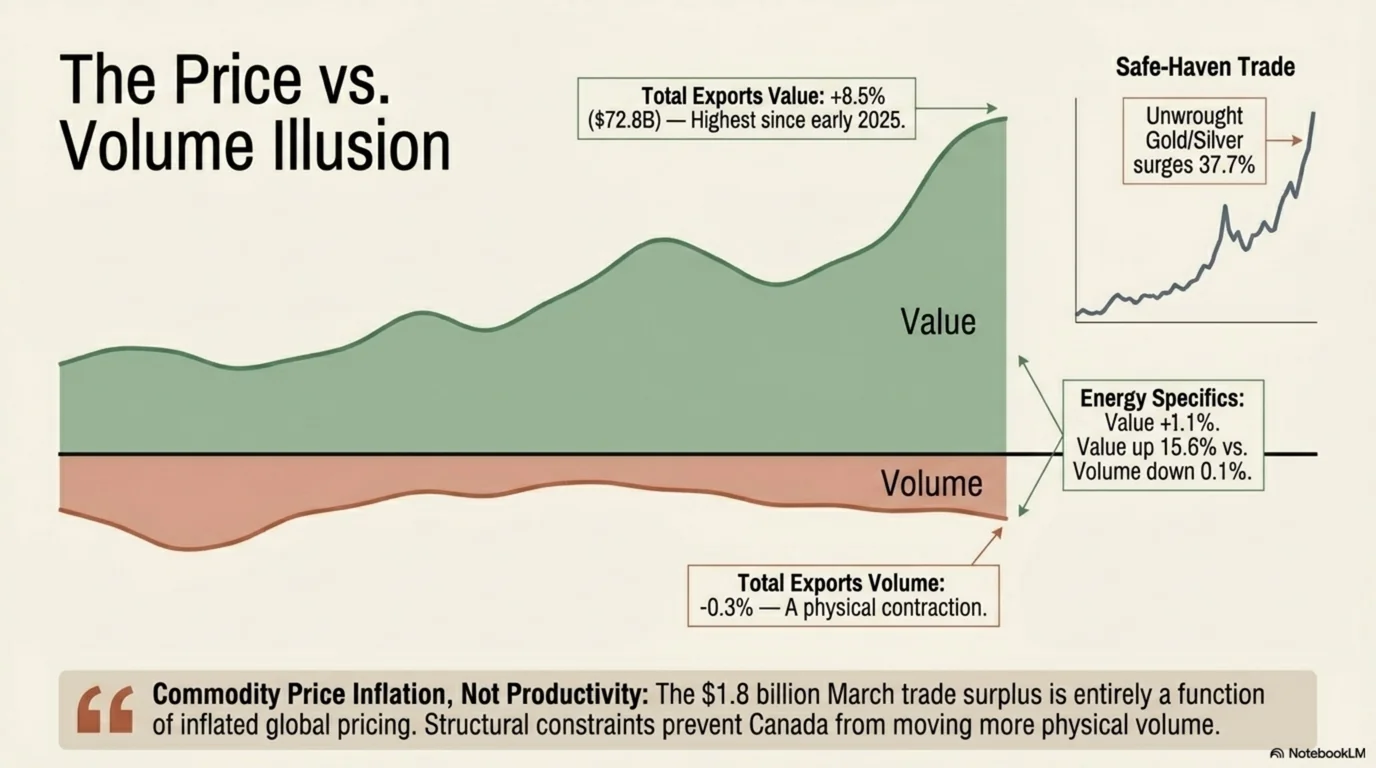

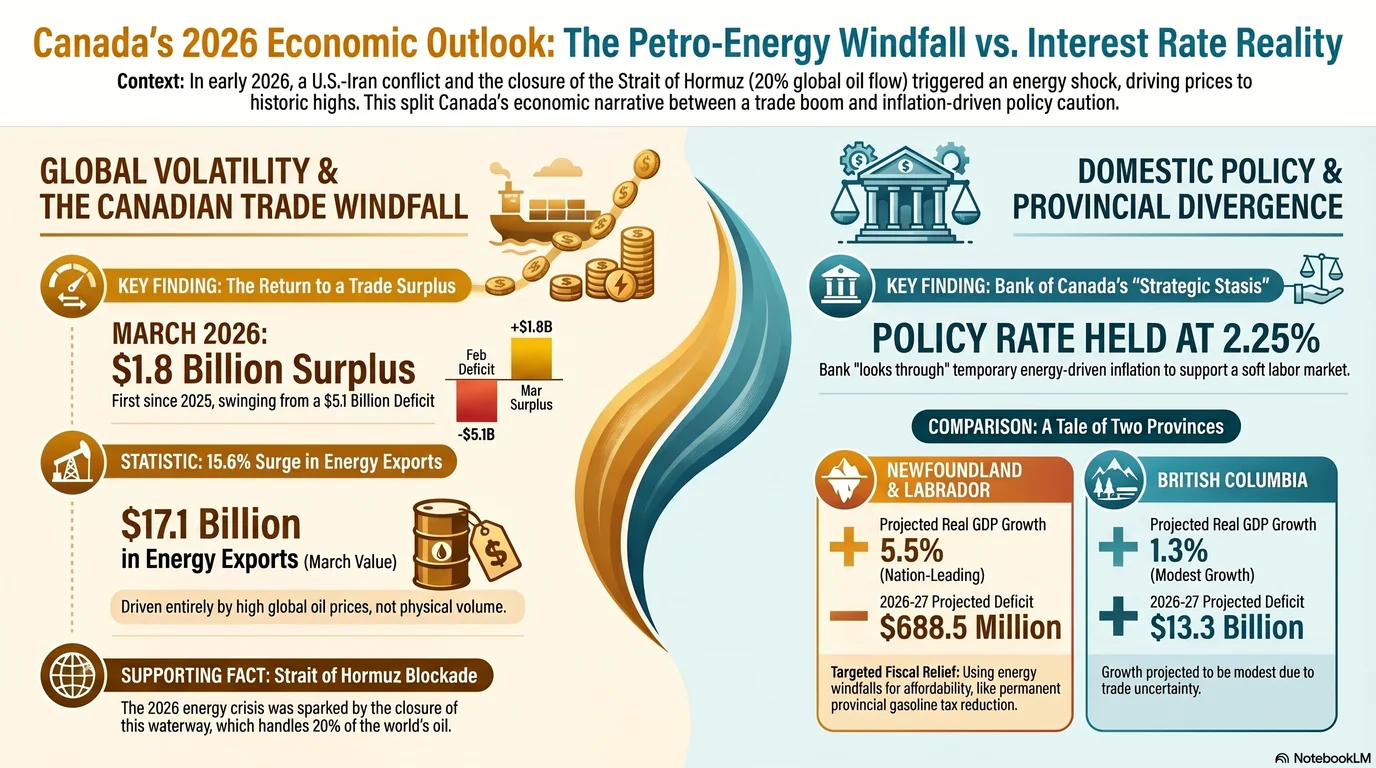

Then came the oil windfall. In a single month, Canada's international merchandise trade balance violently swung from a $5.1 billion deficit in February to a $1.8 billion surplus in March.[19,20]

This miraculous recovery is almost entirely a function of commodity price inflation rather than a sudden boom in physical economic productivity.[20] Total export values surged 8.5% to $72.8 billion, yet physical export volumes actually edged down by 0.3%.[19,20] Energy exports jumped 15.6% to $17.1 billion, driven by an 18.9% spike in the value of crude oil shipments.[21,22] The geopolitical panic also triggered a safe-haven flight to precious metals, pushing Canada's exports of unwrought gold up by 37.7%.[21,23]

The Fiscal Windfall Offsetting Domestic Debt: This surge in national income acts as an impenetrable shield. At the federal level, the Spring Economic Update 2026 explicitly notes that higher crude prices are providing a crucial offsetting boost, with Canada's nominal GDP projected to exceed previous estimates by an astonishing $46 billion in 2026.[24–26] This helps improve the national debt-to-GDP ratio to a highly competitive 41.0%.[27]

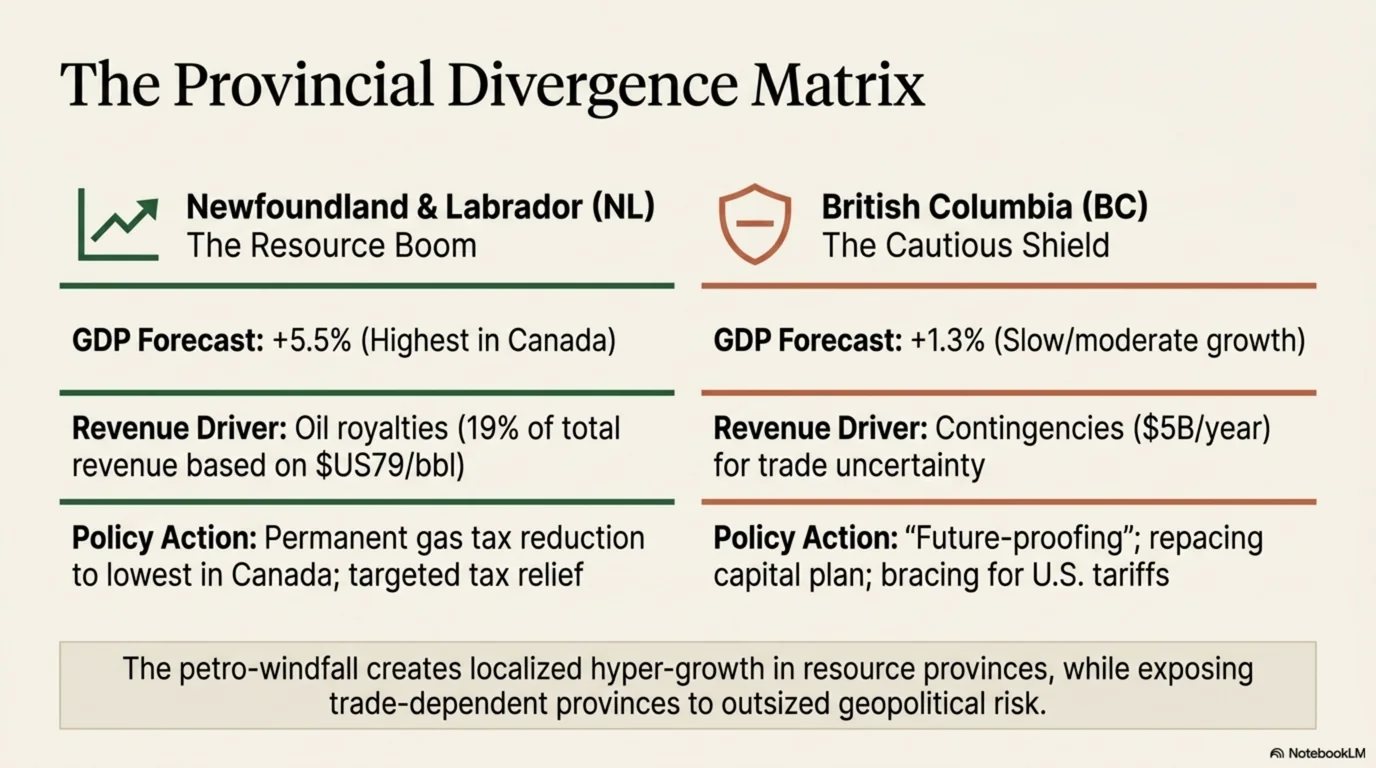

The impact is even more staggering provincially: Newfoundland and Labrador has emerged as the fastest-growing provincial economy, with real GDP forecast to explode by 5.5% in 2026.[28,29] With oil royalties accounting for 19% of the province's overall revenue, the government slashed its provincial gasoline tax to the lowest in the country to directly shield consumers.[29,30] The macro-level influx of foreign capital is propping up the Canadian dollar and giving the Bank of Canada a highly unexpected cushion.

The BoC Dilemma

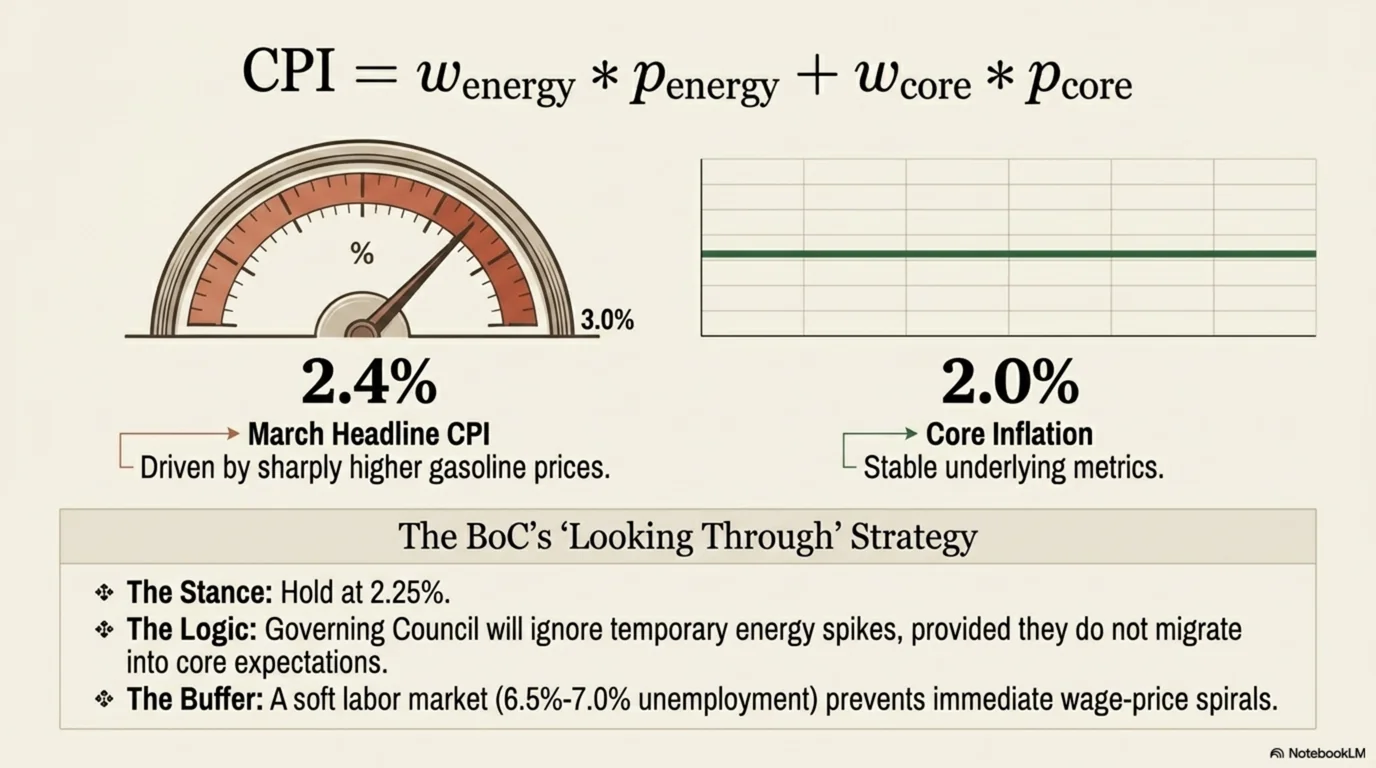

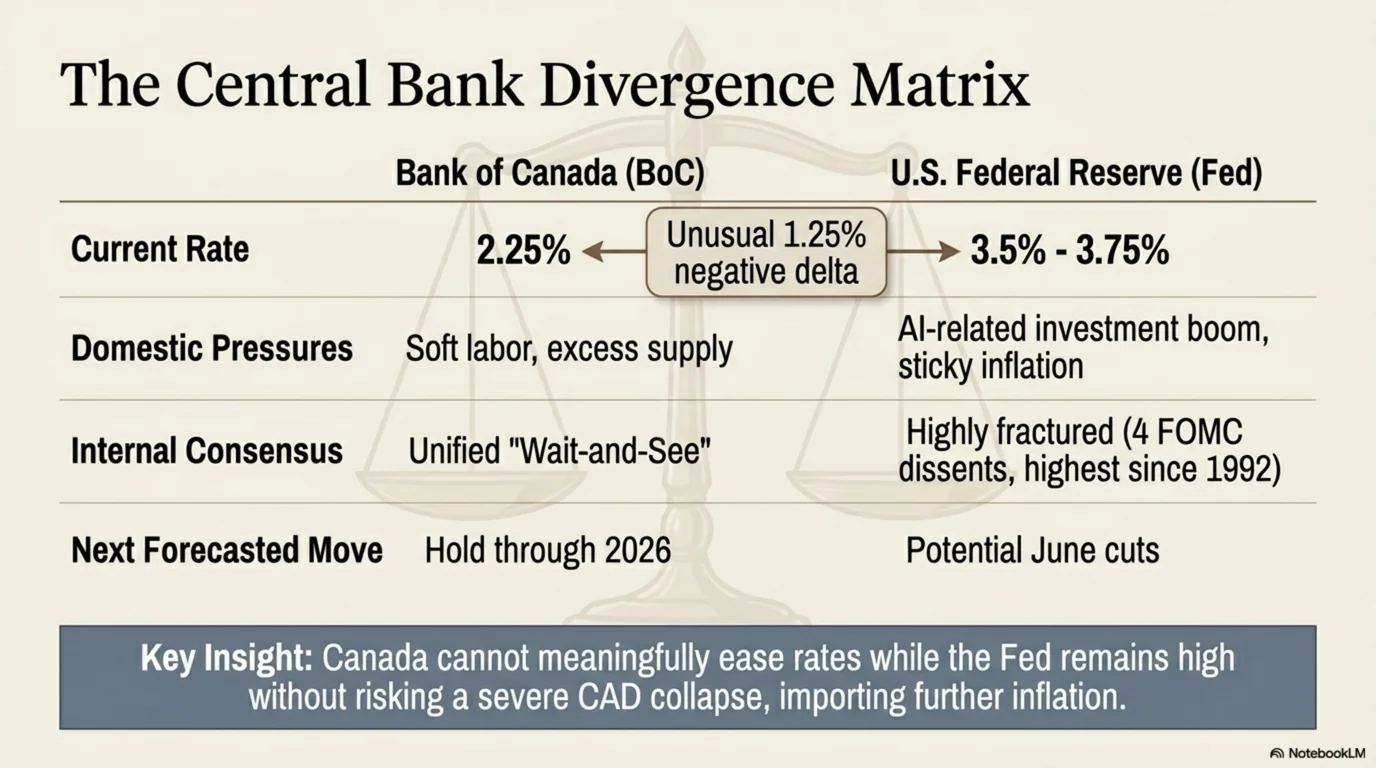

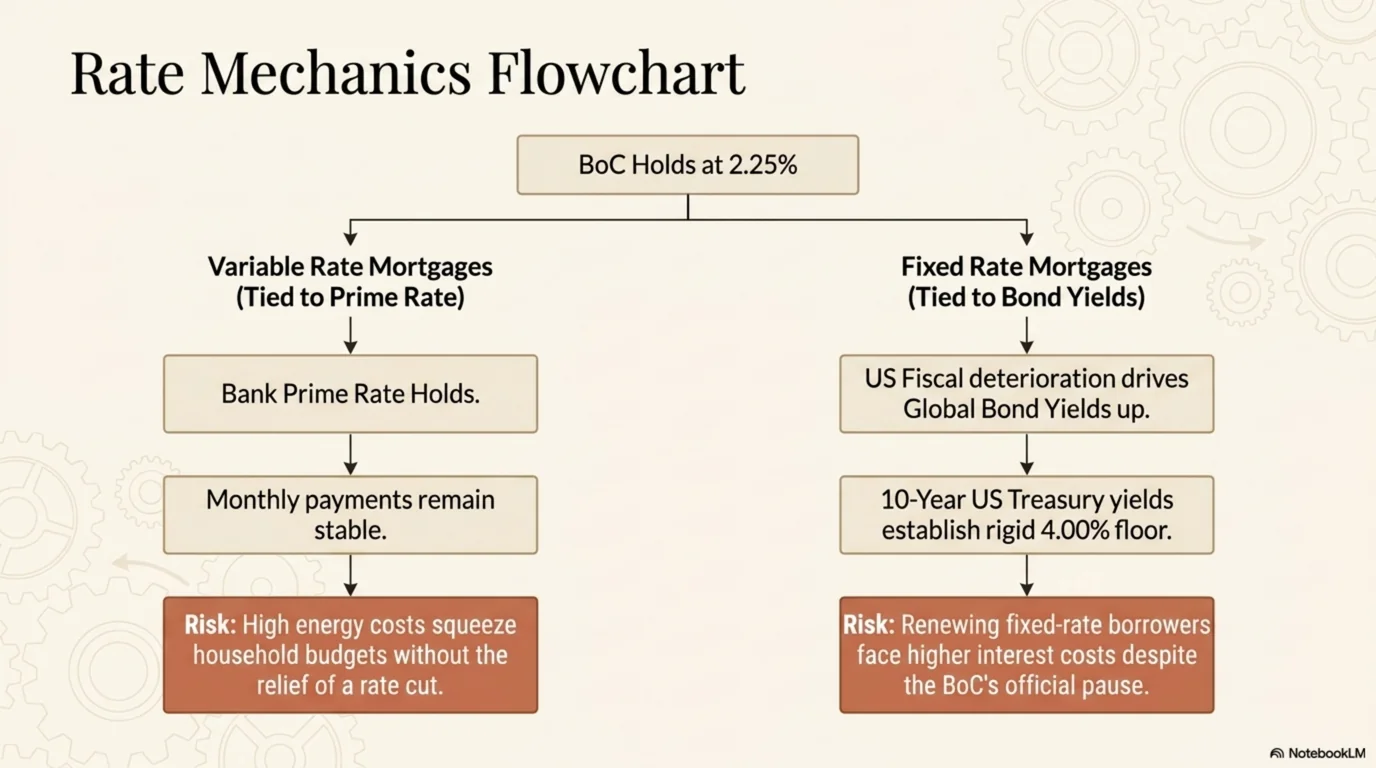

For the Bank of Canada (BoC), the sudden resurrection of the petro-currency is a high-wire macroeconomic balancing act. In April 2026, the BoC opted to hold its benchmark overnight interest rate steady at 2.25%.[18,31] Headline CPI inflation suddenly shot up to 2.4% in March, driven entirely by a historic 21% spike in gasoline prices from the blockade.[32,33] However, core inflation held remarkably steady at roughly 2.25% to 2.3%.[34,35]

This creates a massive policy dilemma for BoC Governor Tiff Macklem, who stated the Governing Council is "looking through the war's immediate impact on inflation".[18,36] Yet, Macklem delivered a stern warning that the BoC will not allow higher energy prices to morph into persistent inflation, noting that if the oil shock drags on, "there may be a need for consecutive increases in the policy rate".[18,36,37]

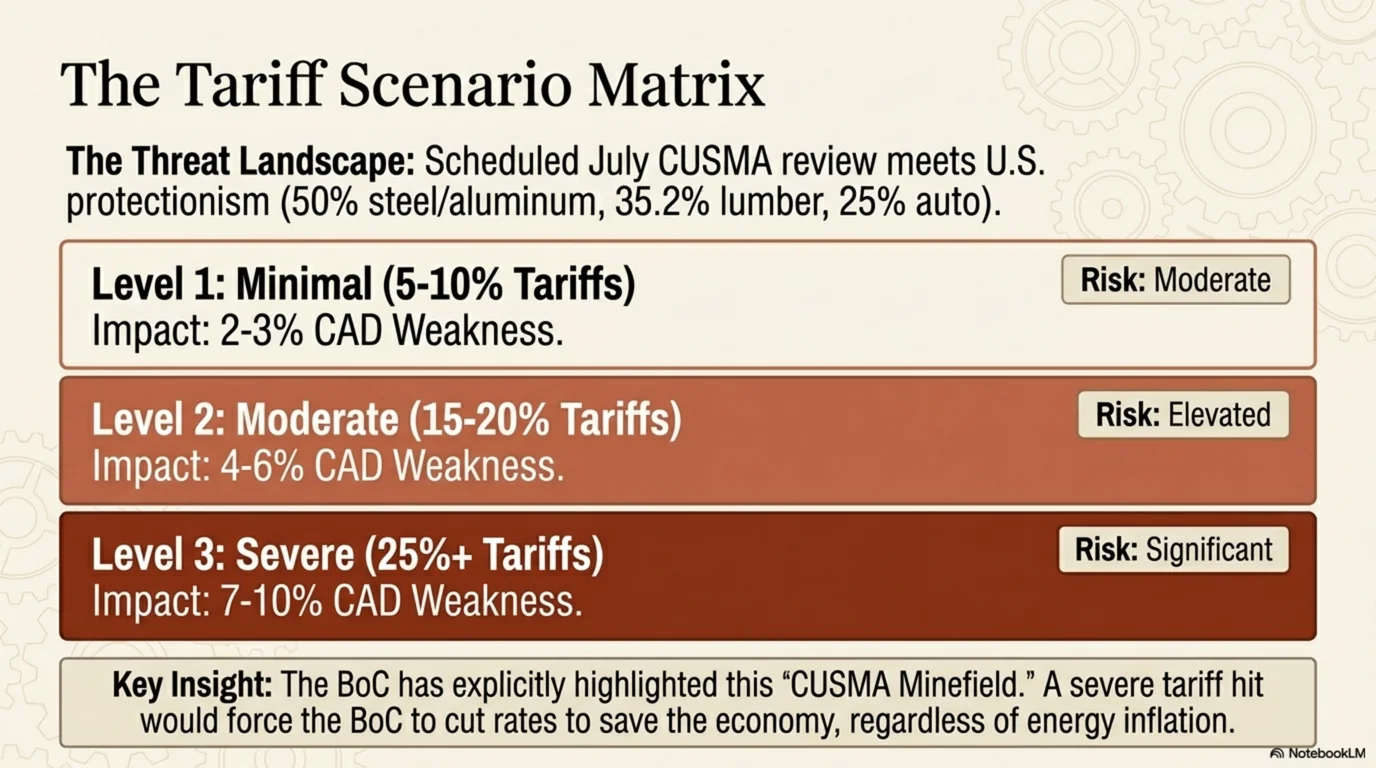

The currency market severely compounds this headache. The U.S. Federal Reserve has kept its target rate in a restrictive 3.50% to 3.75% range, leaving a staggering 1.25% policy gap between the Fed and the BoC.[38,39] In normal conditions, this differential would crush the Canadian dollar, driving severe import inflation and forcing the BoC to hike.[40] Instead, the BoC faces pressure in the opposite direction due to the looming threat of U.S. trade protectionism and the impending CUSMA review.[41,42] If the U.S. imposes significant new trade restrictions, the BoC is prepared to pivot and cut interest rates to support domestic economic growth.[43]

| Date | Central Bank | Rate | Action | Inflation | Context | Outlook |

|---|---|---|---|---|---|---|

| Apr 29, 2026 | Bank of Canada | 2.25% | Held | 2.4% (Mar) | US-Iran war; oil spike; Strait of Hormuz blockade; CUSMA review | Wait-and-see; hike if energy inflation persists, cut if trade hit[1–6] |

| Apr 29, 2026 | Federal Reserve (US) | 3.50–3.75% | Held | 2.5% Core (Jan) | US-Iran war; solid economic activity; AI-related investment | Delayed cuts; stability expected until late 2026, possible easing 2027[2,4,7] |

| May 4, 2026 | Federal Reserve (US) | — | — | — | Middle East crisis; oil volatility; safe-haven USD demand; firm inflation | Cuts delayed; low probability for June, higher for July[8,9] |

| May 4, 2026 | European Central Bank | — | — | 2.0% (target) | Strait of Hormuz disruption; oil above $100/bbl | Aggressive cuts unlikely near-term[8] |

| Apr 30, 2026 | European Central Bank | 2.00% | Held | 1.7% (Euro Area) | Sluggish activity due to high energy prices | Dovish; ready to ease if headline inflation stays low[4,10] |

| Apr 30, 2026 | Bank of England | 5.25% | Held | — | Wafer-thin committee split (8–1) | Uncertain; tension between holding and further easing[4,11] |

| Apr 2026 | Bank of Japan | 1.00% | Increased | 2.4% Core | Yen depreciation; PM fiscal stimulus mandate | Restrictive; targeting 1.25% by July[10] |

| Mar 18, 2026 | Bank of Canada | 2.25% | Held | 1.8% (Feb) | Iran conflict escalation; initial US naval blockade of Iranian ports | Stability; monitoring second-round inflation effects[4,12] |

| Feb 4, 2026 | Reserve Bank of Australia | 3.85% | Increased | — | Q4 inflation pick-up; surge in job growth | Hawkish; another hike expected mid-year[10] |

| Jan 28, 2026 | Federal Reserve (US) | 3.50–3.75% | Held | — | Solid expansion; stabilized unemployment | Gradual easing; rate cuts expected June 2026[10] |

| Jan 28, 2026 | Bank of Canada | 2.25% | Held | — | Adjusting to US protectionism headwinds | Long pause; timing of next move uncertain[10,12] |

Sustainability Audit: The "Gravity" Factor

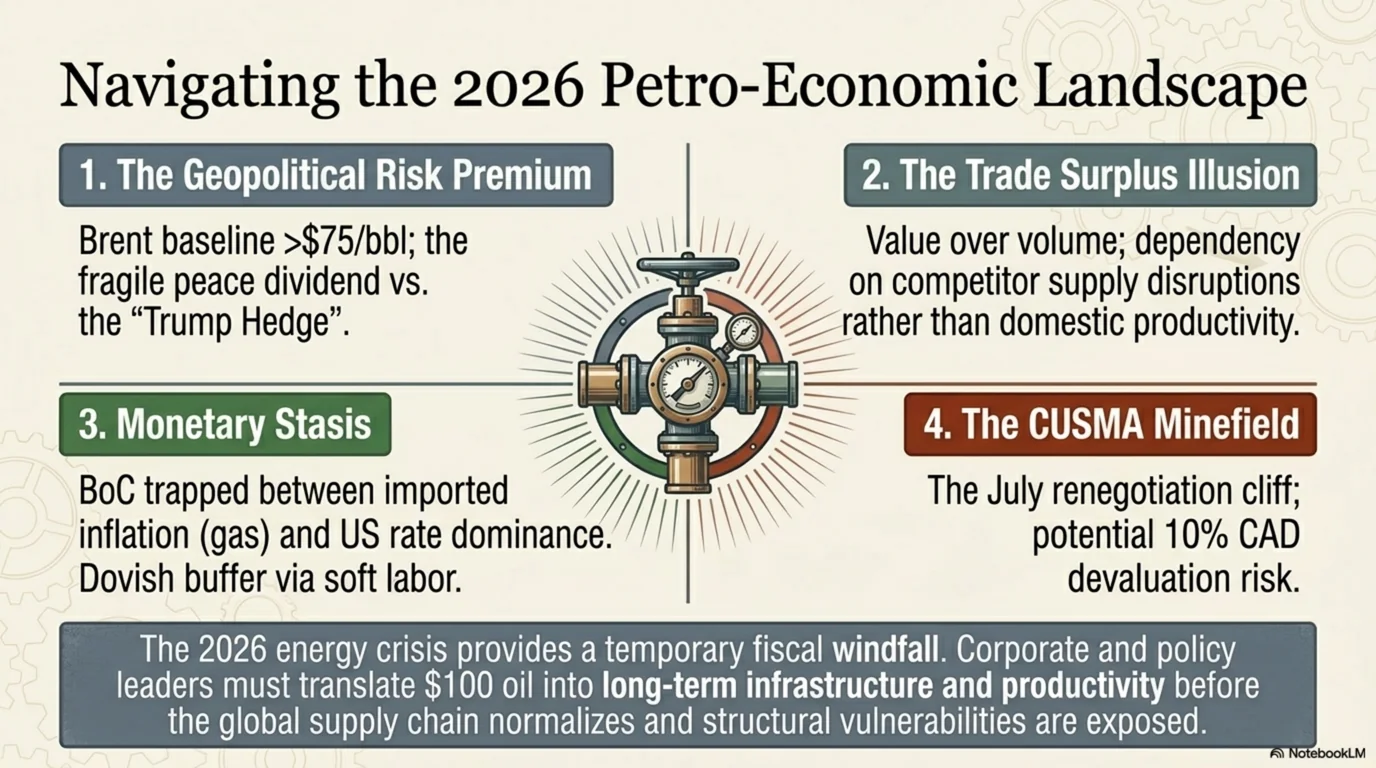

If the oil-driven windfall is keeping the Loonie afloat, what happens when geopolitical winds change? In early May 2026, reports from Axios revealed that Washington and Tehran were closing in on a one-page memorandum of understanding to end the war and reopen the Strait of Hormuz.[44,45] The market reaction was violent: Brent crude plunged 11% to fall below $98 a barrel, while WTI plummeted to near $90.[44,46]

This sudden deflation forces us to ask if the CAD is overvalued based on non-energy fundamentals. The data suggests the CAD is highly vulnerable to gravitational pull if oil prices normalize:

- Lethargic Economic Growth: The Bank of Canada projects a meager 1.2% real GDP growth for 2026.[47]

- The Yield Disadvantage: U.S. 10-year Treasury yields have surged above 4.4%, while Canadian 10-year yields lag around 3.6%, heavily favoring U.S. dollar-denominated assets.[48,49]

- The CUSMA Minefield: The scheduled review of the Canada-United States-Mexico Agreement by July 1, 2026, remains a critical vulnerability.[42,50] Analysts warn that in a "severe tariff scenario" of 25% or more, the Canadian dollar could suffer a devastating 7% to 10% depreciation.[51]

- Exhausted Speculative Momentum: With net short bets against the CAD shrinking from -78.3K to -38.5K by May, the bulk of the short-covering rally is now exhausted, leaving the currency without technical momentum for further appreciation.[6–8]

Conclusion: Forward-Looking Outlook (Through 2026)

As we look toward the final quarters of 2026, the Canadian dollar remains trapped in a volatile tug-of-war between commodity prices and a high-yielding U.S. dollar. Assuming the global economy avoids a total collapse of CUSMA or renewed kinetic war, forecasts from major financial institutions—including RBC, CIBC, BNS, TD, and BMO—all project the USD/CAD exchange rate to end 2026 in the 1.32 to 1.33 range.[52]

However, this mild appreciation requires a highly specific macroeconomic sequence:

- Oil Normalization: Forecasters expect Brent crude to eventually settle into a structurally elevated range of $76 per barrel by 2027 as supply chains are restored, a level that remains highly profitable for the Canadian energy sector.[53]

- Trade Relief: The July CUSMA negotiations must result in an outcome that preserves trade, effectively removing the tariff overhang currently paralyzing investment.[41,54]

- The Fed Pivot: The U.S. Federal Reserve must eventually follow through on delayed rate cuts, narrowing the punishing 1.25% yield gap suppressing Canadian currency strength.[39,40]

Ultimately, the story of the Canadian dollar in 2026 is one of accidental salvation. An unwelcome, inflationary war on the other side of the globe inadvertently handed Canada an economic shield exactly when its domestic economy was fracturing.[1,55] The Loonie has defied gravity masterfully thus far, but as geopolitical fears recede, the currency will eventually have to stand on its own fundamental strength.[54,56]